- Investment Research Partners

- Mar 10

- 10 min read

Executive Summary

On February 28, the United States and Israel launched a joint military operation against Iran (Operation Epic Fury), targeting nuclear facilities, missile sites, and regime leadership. Iran’s Supreme Leader Ayatollah Ali Khamenei was killed in the strikes.[1]

Iran has retaliated with missile and drone attacks against Israel and U.S. military bases across the Gulf region, including targets in Qatar, Kuwait, Saudi Arabia, and the UAE. Seven U.S. service members have been killed as of this writing.[2]

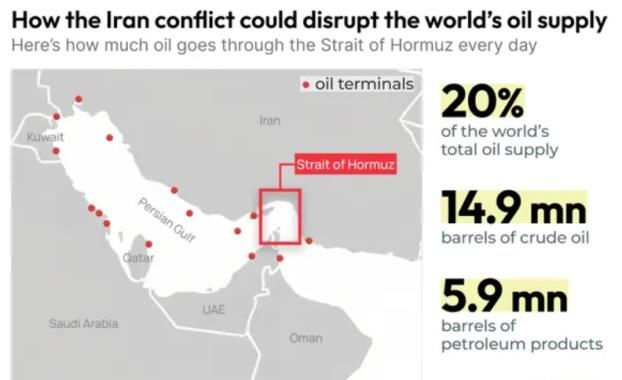

Oil prices have spiked and are trading with significant volatility, with WTI crude rising more than 40% and reaching nearly $120/barrel on Sunday before settling in the mid-$80s on Monday afternoon. The Strait of Hormuz, through which roughly 20% of global oil transits, has been effectively closed for more than a week with timing of resolution still uncertain.[2]

U.S. equity markets initially sold off on Monday, March 2, but recovered by midday. Markets are marginally lower since the conflict began, and the pattern of elevated volatility and trading in sharp swings driven by headlines has continued. The bond market notably did not exhibit a traditional flight to safety trade, with 10-year Treasury yields actually rising slightly.[3]

President Trump has indicated the military operation could last approximately four weeks and is ahead of schedule. The situation remains fluid, but historical precedent suggests markets tend to recover relatively quickly from geopolitical shocks.

What Is Happening?

In the early hours of Saturday, February 28, the United States and Israel launched “Operation Epic Fury,” a coordinated military strike campaign against Iran. The operation targeted Iran’s nuclear enrichment facilities at Fordow and Natanz, ballistic missile production sites, naval capabilities, and regime leadership. The strikes resulted in the death of Supreme Leader Ayatollah Ali Khamenei, who had ruled Iran for over three decades. [1]

The operation followed months of escalating tensions. In June 2025, the U.S. and Israel struck Iranian nuclear facilities in a more limited engagement that ended with a ceasefire on June 23. However, as we covered in our “Geopolitics: Conflict in the Middle East” piece at that time, uncertainty remained about whether Iran’s nuclear program had been fully dismantled. According to the administration, Iran resumed rebuilding its nuclear capabilities and expanded its ballistic missile program in the months following the summer ceasefire, prompting renewed diplomatic efforts in February 2026 that ultimately failed. [4]

Iran has responded with retaliatory strikes against Israel and U.S. military installations across the Gulf, including Al Udeid Air Base in Qatar (the largest U.S. base in the region), as well as targets in Kuwait, Saudi Arabia, and the UAE. Civilian infrastructure in Dubai was also affected. Seven American service members have been killed, with additional casualties expected as the operation continues. The conflict has also expanded to Lebanon, where Israel launched strikes against Hezbollah targets after the group fired projectiles at Israeli military sites. In a signal that Iran is not planning to capitulate, the Islamic Republic announced that Mojtaba Khamenei, the son of the previous supreme leader who was killed in the February 28th attacks, would become the next supreme leader. [1,2]

Why Does This Matter For Markets?

If we focus purely on the market and economic implications of this conflict, the primary impact centers on energy markets. Iran exerts significant influence over the Strait of Hormuz, one of the world’s most critical oil transportation passages. Roughly 20% of the world’s oil supply passes through this narrow waterway. While Iran can’t technically close the strait, given the proximity of ships to shore they can easily launch attacks at passing vessels. Iran has warned ships not to enter the Strait, and major shipping companies including Maersk have suspended vessel crossings until further notice. [5]

Energy Prices Spike

Any extended closure of the Strait of Hormuz could cause significant disruption in energy markets and a further spike in oil prices. Some analysts have estimated that a prolonged closure could drive oil to over $100 per barrel, which would have meaningful inflationary consequences globally.[6] Qatar has also halted liquefied natural gas (LNG) production following Iranian drone attacks, cutting off approximately 20% of global LNG supply and sending European natural gas prices sharply higher.[7]

However, there are several mitigating factors worth noting. First, U.S. and Israeli strikes appear to have significantly degraded Iran’s ability to impact the waterway. Second, eight OPEC+ countries have announced they will boost production by more than 200,000 barrels per day to help offset supply concerns.[8] Third, the United States is far less dependent on Middle Eastern energy than it was during previous conflicts; domestic production has increased dramatically over the past decade, providing. greater energy independence. Iran’s share of global energy production has fallen to around 4%.[9] While this is still significant, it is the potential for disruption through the Strait of Hormuz rather than the loss of Iranian production alone that poses the greatest risk.

How Have Markets Reacted?

The initial market reaction on Monday, March 2, was notable for its restraint. While U.S. futures fell sharply overnight, buyers stepped in erasing losses by midday. The S&P 500 closed essentially flat after being down as much as 1.2% at its lows. The Nasdaq actually gained 0.36%, driven by large-cap tech names.[3] Perhaps more telling than the equity response was the bond market’s reaction. In a traditional “flight to safety,” we would expect investors to rush into Treasuries, pushing yields lower. Instead, long-term Treasury yields actually rose slightly, suggesting that the bond market’s primary concern is the potential inflationary impact of higher oil prices rather than a broader risk-off move.[3]

As hostilities continue, volatility has been elevated as markets have traded in tandem with energy prices and have been moving dramatically on headline developments. Consider the market activity in just one day on March 9th, where the S&P 500 opened sharply lower after WTI crude oil prices spiked to nearly $120/barrel over the weekend. Comments late in the day from President Trump suggesting the war will be over soon led to a dramatic rebound in equities, with the S&P 500 index ending the day up close to 1%, and a reversal in oil prices, with WTI ending the day around $85/barrel.[3,11] The volatility in equities since the conflict began is illustrated in the chart below.

Intraday volatility aside, most major equity markets are modestly lower since the conflict began. The S&P 500 has lost approximately 1%, and the tech-heavy Nasdaq is close to unchanged. International and emerging markets have been weaker, challenged by a higher U.S. dollar.

The sector-level moves were largely predictable with energy stocks, defense contractors, and cybersecurity names rallying. On the other side, airlines, cruise lines, and travel-related stocks fell on flight disruptions and higher fuel cost expectations. Gold spiked initially above $5,300/oz before retreating to pre-strike levels, while oil rose approximately 40%. [3]

Historical Context: Markets & Geopolitical Events

As we have noted in previous geopolitical updates, history suggests that equity markets have generally recovered relatively quickly from military conflicts and geopolitical shocks. Research from JP Morgan looked at 36 geopolitical events from 1940 through Russia’s invasion of Ukraine in 2022 and showed that the S&P 500 posted an average gain of 0.3% three months following a major geopolitical event and six months following an event that returns were the same as the average 6 month return over all time periods.[10]

The chart from First Trust below illustrates the importance of remaining invested over time. It shows the growth of $10,000 invested in the S&P 500 since 1970 through dozens of crises and major events. The average annual total return over this period was 10.94%, and a $10,000 investment grew to over $3.1 million despite wars, recessions, pandemics, terrorist attacks, and financial crises..

Middle Eastern conflicts specifically have a long track record in markets. The table below summarizes several notable examples. While humanitarian impacts can be significant and lasting, financial markets have historically rebounded relatively quickly, with oil prices experiencing the most volatility.

Modern Middle East Conflict – Historical Context

Event | Year | Summary of Impact |

Yom Kippur War | 1973 | Oil embargo caused prices to quadruple; double-digit inflation; bear market in equities and stagflation |

Iran Revolution & Iraq War | 1979 | Oil prices roughly doubled from ~$15 to above $30; central banks raised rates significantly to combat inflation |

Gulf War | 1990 | Oil spiked from ~$15 to ~$40 after Iraq invaded Kuwait but fell back within a year; equities initially sold off then rallied within ~6 months |

Iraq War | 2003 | Oil rose from mid-$20s to ~$40 then declined; equity market reaction was relatively muted |

Arab Spring | 2011 | Libya output fell sharply, sending crude over $120; other suppliers offset; equities volatile |

Drone Attack on Saudi Arabia | 2019 | Abqaiq facility hit, removing 5% of global supply; oil surged ~15% in one day but output resumed within weeks |

Israel – Hamas | 2023 | Oil temporarily rose from $85 to $92 then receded; no significant lasting market impact |

Israel – Iran (June 2025) | 2025 | Initial spike in oil prices and equity volatility, which reversed after ceasefire announced June 23 |

U.S./Israel – Iran (Operation Epic Fury) | 2026 | Ongoing – Oil up ~40%; gold surged above $5,300 before retreating; equities volatile, modestly lower; Strait of Hormuz disruption a key risk |

Source: Ycharts, Bloomberg as of March 9. 2026.

Key Risks & Scenarios To Monitor

While the initial market reaction has been relatively contained, we believe it is important to consider the range of potential outcomes going forward. As with the Ukraine situation we covered in early 2022, the potential outcomes range broadly, from a relatively contained event to something more destabilizing.

If the conflict remains contained (base case): President Trump has indicated the operation could last approximately four weeks and is ahead of schedule. If U.S. and Israeli strikes successfully degrade Iran’s military capabilities, the Strait of Hormuz reopens, and a transition of power in Iran proceeds without prolonged chaos, markets could normalize relatively quickly. OPEC+ production increases could help offset temporary supply disruptions. In this scenario, the conflict may resemble the June 2025 engagement, a short-term disruption followed by recovery.

If the conflict escalates or extends: A prolonged closure of the Strait of Hormuz would provide additional downside risk. Analysts have estimated this could push oil prices to over $100 per barrel, impacting inflation and potentially delaying Federal Reserve rate cuts. Any escalation involving China (Iran’s primary oil buyer) or Russia (a key Iranian ally) would represent a more serious geopolitical shift and likely rattle global markets. Additionally, the political transition in Iran with no clear successor introduces uncertainty that could persist for months.

It is also worth noting that this event does not occur in a vacuum. Markets were already contending with elevated valuations, uncertainty around tariffs and trade policy, ongoing questions about AI-related disruption, and lingering inflation concerns. The broader uncertainty narrative takes on more weight with an active military conflict in the mix.

Our Perspective

As we have stated in previous geopolitical updates, we believe the wise course of action is to stay focused on long-term investment objectives rather than making reactive portfolio changes based on short-term developments. Periods of heightened geopolitical uncertainty can be unsettling. As long-term investors we have found it best to avoid knee-jerk reactions and instead focus on lasting economic and market impacts when making investment decisions.

That said, we are closely monitoring several factors: the status of the Strait of Hormuz and broader energy supply chains; the trajectory of oil prices and their potential inflationary impact; the duration and scope of U.S. military involvement; and any signs of escalation involving other countries. We believe the most likely scenario is that the conflict remains contained, but we are prepared to adjust if circumstances warrant.

We believe that the most successful strategy is to maintain diversification, stay invested, and be ready to evaluate opportunities that periods of volatility can create for long-term investors. As always, please reach out if you would like to schedule a time to review your specific situation.

Sources

[1] Source: CNN, “What we know about the widening US war with Iran,” March 2, 2026

[2] Source: Bloomberg, “Trump Says ‘I Have a Plan’ as War Triggers Tumult in Oil Market, March 9, 2026

[3] Source: Market Data from Bloomberg, YCharts as of March 9, 2026

[4] Source: UK House of Commons Library, “US-Israel strikes on Iran: February/March 2026,” March 3, 2026

[5] Source: GZERO, US Energy Information Administration

[6] Source: Fortune, “Stock market today: Dow futures fall as Trump hints at Iran sanctions relief,” March 1, 2026

[7] Source: Wall Street Journal: “European Gas Prices Soar after Qatar LNG Halt Jolts Market,” March 3, 2026

[8] Source: New York Times, “OPEC Plus to Boost Oil Production as Iran Strikes Threaten Price Spike” March 1, 2026

[9] Source: Tortoise Capital: Middle East Crisis & What it Means for Global Energy Markets, June 24, 2025; RBC Brewin Dolphin

[10] Source: JP Morgan, “How Do Geopolitical Shocks Impact Markets” 2024

[11] Source: Bloomberg, “Stocks Climb as Trump Hints War Could Be Over Soon,” March 9, 2026

Important Disclosures

Past performance may not be representative of future results. All investments are subject to loss. Forecasts regarding the market or economy are subject to a wide range of possible outcomes. The views presented in this market update may prove to be inaccurate for a variety of factors. These views are as of the date listed above and are subject to change based on changes in fundamental economic or market-related data.

All data and information reference herein are from sources believed to be reliable. Any opinions, news, research, analyses, prices, or other information contained in this research is provided as general market commentary, it does not constitute investment advice. Investment Research Partners shall not in any way be liable for claims, and makes no expressed or implied representations or warranties as to the accuracy or completeness of the data and other information, or for statements or errors contained in or omissions from the obtained data and information referenced herein. The data and information are provided as of the date referenced, and such data and information are subject to change without notice. Certain third-party sources cited in this material may require a paid subscription or may otherwise be located behind a paywall. If you would like more information regarding any cited source, please contact IRP and we will provide additional details upon request. Please contact your Advisor in order to discuss your specific situation.

IRP employs artificial intelligence using a number of platforms for the purpose of researching investments and comparing various investment platforms. IRP has evaluated the security of these AI platforms, and does not use any platform that uses client information to train its models or that maintains sensitive client information in its records. Further, human input is required by IRP policy to ensure accuracy of the information generated by AI, and any data aggregation or document summaries. The use of these platforms will be reviewed periodically to ensure confidentiality and accuracy as well as efficiency.

.png)